Delivering affordable healthcare benefits has never been more critical, or more complex. Prescription drug prices continue to rise faster than wages, widening the gap between cost and access. Employees are increasingly forced to make difficult trade-offs between their health needs and everyday household expenses.

For employers, the implications extend far beyond health plan budgets. High cost medications and specialty treatments, including newer weight management and metabolic health therapies, are placing growing pressure on traditional benefit models. As demand rises, organizations are navigating difficult questions around access, equity, and sustainability, all while trying to maintain employee trust and engagement.

As HR leaders rethink the role of benefits in supporting the modern workforce, one theme stands out. Flexibility is no longer a perk. It has become a strategic response to rising healthcare costs and evolving employee expectations. The challenge is no longer simply how to contain spend, but how to design benefits that preserve affordability, strengthen trust, and support wellbeing in a healthcare landscape that feels increasingly out of reach.

Here’s what we’ll cover:

- Why healthcare affordability is the next frontier of HR strategy

- How cost pressures are reshaping benefit philosophy

- GLP-1 medications and specialty drugs are reshaping employer healthcare spend

- Financial wellness as a foundation for workforce resilience

- Benefit design levers that HR can pull

- Specialty allowances: support in an evolving benefits landscape

- What 2025 benefit trends reveal about the future of flexibility

- Building a culture of care: leadership lessons for HR

- From cost management to human-centered strategy

Why healthcare affordability is the next frontier of HR strategy

Prescription drug costs have become a leading indicator of workforce strain. In 2025, specialty medication prices rose nearly 8%, outpacing wage growth by more than double. For employees, this translates into difficult choices: skipping doses, delaying care, or absorbing new debt. For employers, it signals a deeper cultural risk—the erosion of psychological safety and financial trust among employees.

With healthcare costs projected to rise another 9% in 2026, driven largely by pharmacy spend and the growing use of GLP-1 medications, HR leaders face mounting pressure to balance affordability with access. HR now stands at a crossroads. Traditional benefit levers—plan design, co-pays, and deductibles—can no longer absorb cost volatility. The next generation of benefits must be adaptive, equitable, and empathetic.

As employer healthcare spend continues to rise—driven disproportionately by specialty drugs and GLP-1 medications—HR leaders are realizing that affordability challenges are no longer solvable through plan design alone. What’s emerging instead is a defined, employer-funded approach to specialty care that creates cost containment without cutting access.

When choice replaces control, benefits become a two-way contract: employees feel cared for, and employers gain predictability, equity, and deeper trust.

How cost pressures are reshaping benefit philosophy

Flexibility is the new architecture of affordability. In Willis Tower Watson’s 2025 Benefits Trends Survey, 90% of U.S. employers identified rising benefit costs as a primary influence on their strategy, and many are shifting spend rather than expanding offerings.

Organizations are experimenting with flexible benefit models. Allocating dollars into choice-based accounts or stipends so employees can prioritize what matters most, whether it’s prescriptions, family care, wellness, or preventive services. This shift signals a move away from rigid cost sharing toward empowering employees with choice and autonomy. When choice replaces control, benefits become a two-way contract: employees feel cared for, and employers gain predictability, equity, and deeper trust.

GLP-1 medications and specialty drugs are reshaping employer healthcare spend

GLP-1 medications and other specialty drugs are now among the fastest-growing drivers of employer healthcare spend. While employee demand for weight management and metabolic health support continues to rise, adding these treatments directly to medical plans often results in open-ended claims exposure and long-term benefit cost escalation.

To address this, many employers are adopting Specialty Care Accounts—a healthcare cost containment approach that allows organizations to support GLP-1s, weight management programs, and other specialty treatments through capped, employer-defined allowances, rather than unpredictable medical claims.

This is why many employers are moving GLP-1s and other specialty drugs out of the medical plan entirely, using Specialty Care Accounts to regain control over healthcare spend while still supporting employee access to care.

Financial wellness as a foundation for workforce resilience

Financial wellness is quickly emerging as a cornerstone of workforce sustainability. WTW research shows that nearly two-thirds of employees feel stressed about their finances, and those under financial strain are twice as likely to report disengagement or poor health.

Rising healthcare costs don’t just strain benefit budgets—they directly undermine financial wellness, especially when specialty drug costs fall on employees through higher out-of-pocket expenses.

When medical costs rise faster than pay, this stress compounds. Forward-thinking organizations are addressing it head-on by integrating financial wellbeing into their benefit ecosystems. From budgeting tools and savings incentives to credit-building supports.

While Lifestyle Spending Accounts (LSA) can’t be used for healthcare-covered medical expenses, they play a vital role in reducing everyday financial pressure, which in turn supports better overall wellbeing. Financial security and health are interconnected: employees who feel in control of their finances are more likely to participate in preventive care, stay healthy, and remain loyal to their employer. In an era defined by economic uncertainty, financial confidence is becoming a leading indicator of organizational health.

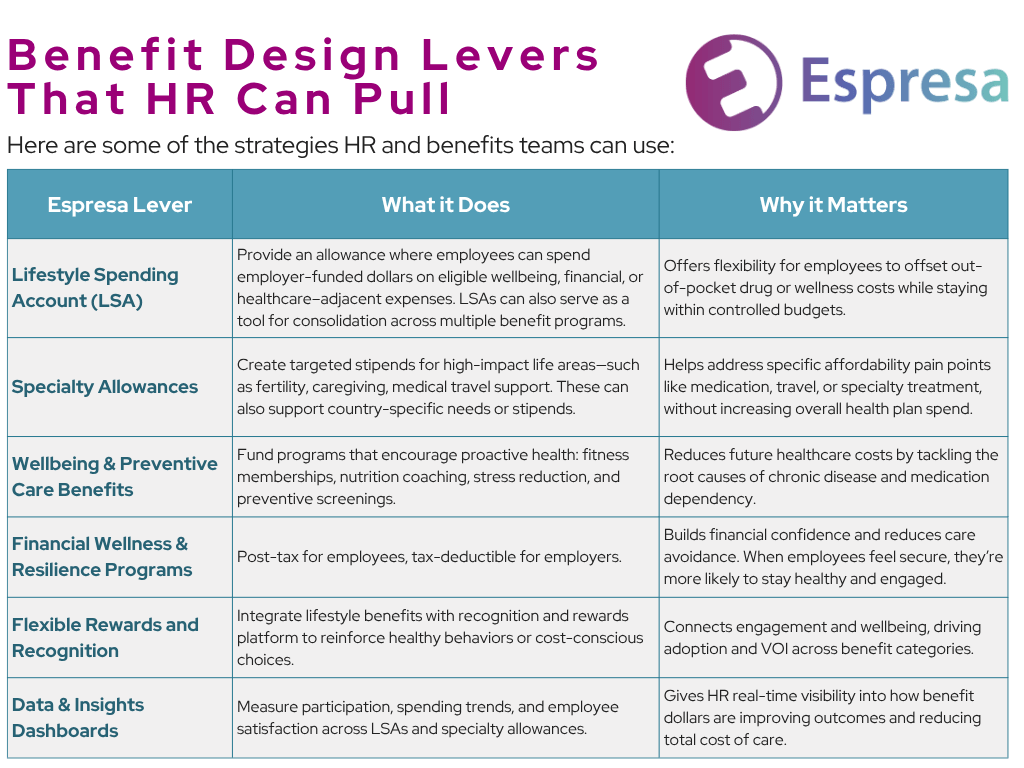

Benefit design levers that HR can pull

As the cost curve steepens, HR teams are redefining what proactive benefit management looks like. The most effective strategies blend financial, physical, and emotional wellbeing into one framework, giving employees flexibility while keeping employer costs predictable and controllable.

The chart below highlights several proven levers HR leaders are using to close affordability gaps, drawn from Espresa’s latest data on flexible benefit adoption.

Specialty Care Accounts are emerging as a critical benefit design lever for organizations seeking to control healthcare costs. By shifting high-cost categories—such as GLP-1 medications, hormone replacement therapy (HRT), and specialty mental health—out of the medical plan and into a defined allowance, employers gain cost predictability while employees retain choice and access.

Specialty allowances represent a maturing benefits philosophy: one rooted in relevance, inclusivity, and intentional design. By aligning benefits with lived experience, employers signal understanding that health and wellbeing are personal, not transactional.

Specialty allowances: support in an evolving benefits landscape

As healthcare costs diversify, benefit design must evolve beyond broad-based coverage to targeted, equitable support. Specialty allowances—targeted stipends for specific life events or circumstances—are becoming a defining feature of modern benefit design. Employers are using them to address needs such as fertility, medical travel, caregiving, or medically-necessary travel, areas often underserved by traditional insurance plans.

Rather than adding layers of programs, these allowances redirect resources to where they have the most tangible impact. They enable employees to navigate high-cost or sensitive health events with dignity, while allowing organizations to maintain predictability and cost discipline while employees maintain privacy and security.

Specialty allowances represent a maturing benefits philosophy: one rooted in relevance, inclusivity, and intentional design. By aligning benefits with lived experience, employers signal understanding that health and wellbeing are personal, not transactional.

How Employers Are Containing Healthcare Costs Without Cutting Benefits

Learn how Specialty Care Accounts help organizations manage employer healthcare spend, control specialty drug costs, and support GLP-1 and weight management programs—without adding long-term claims exposure.

What 2025 benefit trends reveal about the future of flexibility

Across industries, flexibility has moved from experiment to expectation. Recent employer data shows a decisive shift towards benefits that are modular, choice-based, and responsive to employee needs. Nearly 9 in 10 employers now consider health and wellbeing benefits central to their people strategy. Yet participation in traditional wellness programs continues to decline, signalling a move away from rigid structures toward personalization and self-direction.

Flexible stipends and lifestyle benefits have emerged as preferred mechanisms for delivering personalization. Adoption rates are accelerating, with organizations reframing benefits as ecosystems of choice rather than static offerings. These programs enable employees to allocate funds toward supporting their unique wellbeing—from family care to preventive health or prescription costs—while allowing employers to manage cost volatility with clarity and equity.

Key insights from 2025 benefit data illustrate this transformation:

- 68% of employers now offer an LSA or specialty allowance, up from 42% in 2023

- Engagement rates exceed 80% across flexible benefit programs, even amidst tighter budgets

- Personalization has overtaken cost as the top driver of employee satisfaction with benefits

- Financial wellbeing programs are expanding within flexible frameworks, supporting budgeting, savings, and debt management alongside physical and emotional health

- Core health benefits remain critical:

- 88% of employers rate them as “extremely” or “very” important, according to SHRM

- Yet only 39% of organizations now offer structured wellness programs (down from 53% in 2021), reflecting a transition from prescriptive to self-directed care

Together, these trends mark a shift from benefits that are offered to benefits that are employee-led. Flexibility is more than adding options; it’s about redistributing agency.

Building a culture of care: leadership lessons for HR

The rising cost of healthcare has forced HR to evolve beyond benefits administration and into benefits equity. In an environment where affordability, equity, and trust intersect, the design of personal benefits becomes a direct reflection of how an organization values its people.

3 lessons stand out as HR navigates this new challenge:

1. Equity begins with design

True benefit equity is about intentional design that meets people where they are. Programs should reflect diverse life stages, health needs, and family structures, ensuring that flexibility isn’t a privilege only some employees receive.

2. Choices drive engagement

When employees have a voice in how benefits are shaped, such as with surveys, participation becomes ownership. Shared decision-making turns benefits from a corporate offering into a shared experience.

3. Transparency sustains trust

Clear communication about how benefits are prioritized and funded is essential. Particularly when trade-offs are required. Employees don’t expect unlimited resources, but they do expect honesty. HR leaders who explain why certain programs are chosen, or why adjustments are made, cultivate understanding rather than doubt.

Together, these practices reimagine HR leadership as a partnership between the organization and its people. One that moves beyond managing plans to co-creating a culture of wellbeing and fairness.

From cost management to human-centered strategy

Healthcare inflation will continue to test the limits of traditional benefit models. This pressure is also accelerating innovation, pushing HR leaders to move beyond cost control toward human-centered strategy.

The future of benefits lies in integration and intent: connecting health, financial, and emotional wellbeing into one adaptable ecosystem that reflects organizational values. When benefits are aligned through equity, transparency, and empathy, they stop functioning as separate programs and start communicating a unified message: People come first.

For HR, this moment redefines purpose. The future of benefits will be shaped by deliberate organizational spending. Those that lead with flexibility and authenticity will not only weather volatility, they’ll help their people thrive through it.

Employer Healthcare Cost Containment: Frequently Asked Questions

What are the biggest drivers of rising employer healthcare costs?

The biggest drivers of rising employer healthcare costs include specialty drugs, GLP-1 medications, weight management treatments, increased pharmacy utilization, and higher out-of-pocket costs that delay care and drive future claims. These factors are accelerating healthcare spend beyond traditional cost-control mechanisms.

How can employers control specialty drug costs?

Employers can control specialty drug costs by funding access through defined, employer-funded programs—such as Specialty Care Accounts—instead of absorbing ongoing claims through the medical plan. This approach allows employers to cap spending while still supporting employee access to specialty care.

What is the difference between covering GLP-1s through a medical plan vs. a specialty allowance?

Covering GLP-1 medications through a medical plan creates open-ended claims exposure and long-term renewal risk. Funding GLP-1s through a specialty allowance, such as a Specialty Care Account, allows employers to support weight management while maintaining predictable, capped healthcare spend.

Can employers support hormone replacement therapy (HRT) without increasing claims risk?

Yes. Employers can support hormone replacement therapy (HRT) by offering access through Specialty Care Accounts rather than adding coverage to the medical plan. This provides support for menopause and hormonal health while keeping benefit costs controlled and predictable.

How do Specialty Care Accounts differ from traditional stipends?

Unlike traditional stipends, Specialty Care Accounts are designed specifically for healthcare cost containment. They focus on high-cost specialty care categories—such as GLP-1s, specialty drugs, weight management, and HRT—within a structured, employer-controlled framework.

Are Specialty Care Accounts compliant with healthcare benefit regulations?

Specialty Care Accounts can be designed to align with applicable healthcare and tax regulations, depending on program structure. Employers typically implement them alongside existing benefits to ensure compliance while addressing specialty care cost pressures.

Why are employers shifting to defined contribution healthcare strategies?

Employers are shifting to defined contribution healthcare strategies to manage rising benefit costs, reduce volatility, and improve cost predictability. Defined contribution models—like Specialty Care Accounts—offer a sustainable alternative to open-ended medical claims.

How can employers control GLP-1 costs?

Employers can control GLP-1 costs by funding access through capped Specialty Care Accounts rather than adding GLP-1 medications directly to the medical plan.

What is a Specialty Care Account?

A Specialty Care Account is an employer-funded benefit designed to support high-cost specialty care—such as GLP-1 medications, hormone replacement therapy (HRT), specialty mental health, and weight management—through a capped, predictable allowance rather than open-ended medical claims.

How can employers reduce healthcare spend without cutting benefits?

Employers can reduce healthcare spend by shifting high-cost categories—such as specialty drugs, GLP-1 medications, and weight management programs—out of traditional medical plans and into defined, employer-funded programs like Specialty Care Accounts. This approach creates predictable benefit costs while preserving employee access to care.

Why are GLP-1 medications driving employer healthcare costs?

GLP-1 medications are driving employer healthcare costs due to rapid adoption, long-term treatment duration, and limited coverage controls within traditional medical plans. As demand for weight management and metabolic health solutions grows, many employers are seeking healthcare cost containment strategies that avoid ongoing claims exposure.

How can employers manage GLP-1 and weight management benefits responsibly?

Employers can manage GLP-1 and weight management benefits by offering access through Specialty Care Accounts instead of adding them to the medical plan. This allows organizations to support employee demand while maintaining control over benefit costs and avoiding future renewal volatility.

What types of specialty drugs can be covered through Specialty Care Accounts?

Specialty Care Accounts can support a range of specialty drugs and services, including GLP-1 medications, hormone therapy (HRT), menopause care, specialty mental health treatments, and other high-cost or emerging care categories aligned with an employer’s benefits strategy.

How do Specialty Care Accounts support healthcare cost containment?

Specialty Care Accounts support healthcare cost containment by replacing unpredictable claims-based spending with defined, employer-controlled allowances. This structure gives employers visibility into healthcare spend while allowing employees flexibility in how they access specialty care.

Are Specialty Care Accounts part of a broader benefits cost strategy?

Yes. Specialty Care Accounts are often used alongside medical plans and Lifestyle Spending Accounts (LSA) as part of a broader benefit cost strategy. Together, these programs help employers balance rising healthcare costs, employee expectations, and long-term financial sustainability.

Why are employers moving away from traditional healthcare cost-sharing models?

Traditional cost-sharing models—such as higher deductibles and co-pays—shift costs to employees without reducing overall healthcare spend. Many employers are moving toward defined contribution approaches, like Specialty Care Accounts, that provide cost containment while maintaining trust, access, and equity.